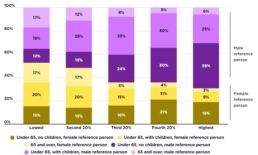

Profile of each income group by gender of household reference person

Families with a female reference person generally have lower incomes than those with a male reference person. The two charts below show the profile of each income group by the gender of the household reference person. 2019-20 This chart shows that a clear majority (70%) of households in the highest 20% income group had a male reference person. 2017-18 This chart shows that the majority (71%) of households in the highest 20% income group had a male reference person.

Community attitudes: Poverty is a problem that can be solved

This chart shows the responses in our Community attitudes towards poverty and inequality survey 2023 to the idea that Poverty is a problem that can be solved. It shows that 75% of people in Australia agreed that poverty is a problem that can be solved with the right systems and policies. Read the full report here: https://bit.ly/communityattitudes2023

Comparison of poverty trend and SDG target path

This chart shows the percentage of people in poverty between 1999-20 to 2019-20 and compares this with the percentage of people in poverty if we were following the target set out in the UN Sustainable Development Goals, of which Australia is a signatory. The Sustainable Development Goal on poverty includes: "By 2030, reduce at least by half the proportion of men, women and children of all ages living in poverty in all its dimensions according to national definitions" (note that this chart uses 50% of median income in lieu of an accepted national definition of poverty in Australia).

Poverty lines by family type

This table shows poverty lines by family type in dollars per week, including social security payments.

Percentage of all people in poverty from 1999 - 2019

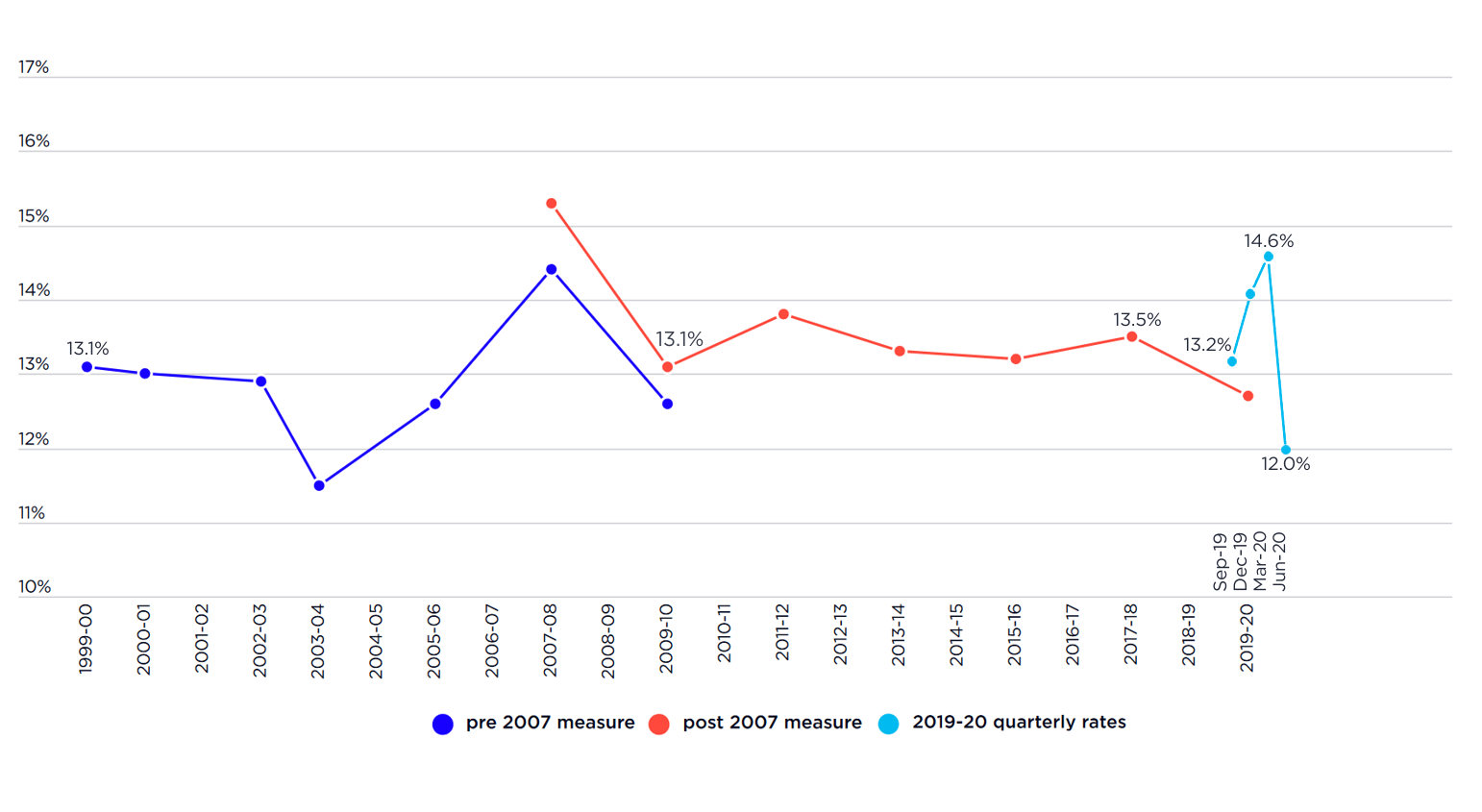

This graph shows the percentage of all people in Australia in poverty from 1999 - 2019. The poverty line used is 50% of median income, taking account of housing costs. The lower (dark blue) line shows poverty rates measured using the pre-2007 ABS income definition, while the higher (red) line is based on the post 2007 income definition. The light blue line shows the quarterly changes in poverty rates during the 2019-20 period, when the impacts of COVID-19 lifted the poverty rate from 13.2% in the September quarter of 2019 to 14.6% in the March quarter of 2020, and the extra coronavirus income support payments introduced meant it fell to 12% - a 17 year low - in the June quarter of 2020.

This graph shows the percentage of all people in Australia in poverty from 1999 - 2019. The poverty line used is 50% of median income, taking account of housing costs. The lower (dark blue) line shows poverty rates measured using the pre-2007 ABS income definition, while the higher (red) line is based on the post 2007 income definition. The light blue line shows the quarterly changes in poverty rates during the 2019-20 period, when the impacts of COVID-19 lifted the poverty rate from 13.2% in the September quarter of 2019 to 14.6% in the March quarter of 2020, and the extra coronavirus income support payments introduced meant it fell to 12% - a 17 year low - in the June quarter of 2020.

Average wealth per adult in 2020

According to Credit Suisse’s Global Wealth Report, the average wealth of Australian households was $628,000 per adult in 2020, the fourth highest in the world behind Switzerland, the United States and Hong Kong (North America as shown on the graph refers to the region, as does Asia-Pacific and Europe).

Average wealth of households by age, as a percentage of the average wealth of all (%)

This graph shows that wealth inequality has increased across generations since 2003, especially in the distribution of owner-occupied housing. As a proportion of the average value of owner-occupied homes held across all age groups: • The average value held in households with a reference person under 35 years fell from 31% in 2003 to 26% in 2021; • That of those aged 35-44 years fell from 82% in 2003 to 69%; • That of those aged 64 years rose from 140% in 2003 to 144%.

Share of wealth held by households ranked by wealth (% in 2021)

Consistent with the findings of our Inequality in Australia 2020 report, wealth is still very unequally distributed in 2021-22. * The highest 10% of households by wealth has an average of $6.1 million or 46% of all wealth. *The next 30% have an average of $1.7 million or 38% of all wealth. * That leaves the majority – the lower 60% - with $376,000 or just 17% of all wealth.

Wealth inequality (Gini coefficient)

This graph shows trends in a summary measure of inequality, the ‘Gini coefficient’. The Gini varies across a range from zero (equal wealth) to one (where all wealth is held by a single household). It rose sharply from 0.573 in 2003 to 0.624 in 2018; and then declined slightly to 0.613 by 2021, close to the level reached around 2016.

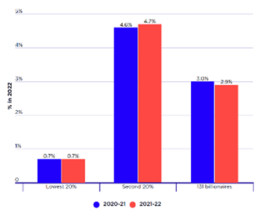

Share of all wealth held by 131 billionaires compared with low-wealth groups (%)

The 131 billionaires comprised 0.001% of the population yet held 2.9% of all household wealth in 2021, a decline from 3% in 2020. This graph shows that they held more wealth among them than the lower 20% of households ranked by wealth (who held 0.7% of all wealth) and somewhat less than the second-lowest 20% (with 4.7%). This suggests that 131 individuals held almost as much wealth between them as the 2.8 million households in the lowest 30% ranked by wealth.